This is the first post in a three-part series where I'll be sharing about my approach to retirement planning! Read on to get the download link for a retirement funds calculator that I have created to project CPF contributions up till age 55/65.

- Central Provident Fund (CPF): Maximize that "free" interest to build your retirement savings

- Supplementary Retirement Scheme (SRS): Short-term liquidity vs Long-term growth

- Investment Portfolio: Meet evolving needs over time

Overview: I plan to use my CPF monies as the most basic level of retirement funds (via CPF Life) from age 65 onwards. The monthly payouts will then be supplemented by withdrawals from my SRS account and dividend payouts (and drawdown on investment capital if necessary) from my investment portfolio.

CPF: Maximize that "free" interest to build your retirement savings

Due to our circumstances, my partner and I are not eligible for a HDB loan or BTO or any of those spoil market (I say this in jest) housing grants. We will be getting a bank loan for our HDB which requires a hefty 25% downpayment. Private housing is totally out of our reach and a mid-priced resale flat is the limit of what we can afford.

Given the hefty downpayment, we will not have much in our OA accounts once the downpayment has been paid. We estimate our monthly loan payment, paid over 25 years, to be roughly $1,600. Split between the two of us, that's $800 per person. With the bulk of our OA contributions going to pay off this house loan during this 25 year period, the funds in our OA will grow at a much slower pace. Therefore, the brunt of retirement savings in our CPF accounts will fall on our SA accounts.

Before I get into the calculations, a few things to keep top of mind:

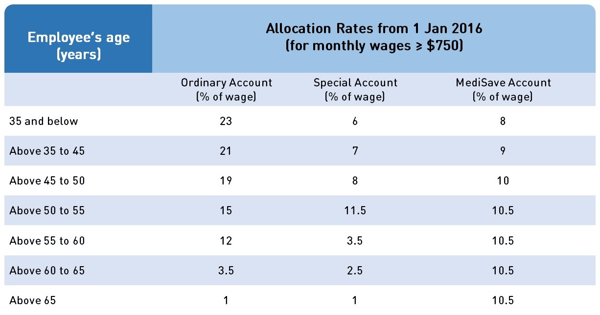

- SA earns 4% interest p.a. (+ 1% on first 40k)

- OA earns 2.5% interest p.a. (+ 1% on first 20k)

- 6-8% of your salary goes into SA (up till age 50)

- Interest is computed monthly and compounded annually (i.e. interest "earnings" are only credited at the start of the next year

- At age 55, SA and OA are merged to form the RA account. The SA is depleted first so if your SA + OA > FRS, any excess largely stay in the OA. RA earns 4% interest p.a. (+ 1% on first 30k)

My CPF Projections

At this point in time, we do not have clarity on the Basic Retirement Sum (BRS) or Full Retirement Sum (FRS) for years 2021 and beyond, but let's take the figures listed on this Dollars and Sense article as a reference. Let us assume a 3% annual increment in salary to match the FRS figures compounded by 3% (rounded to nearest 100). These are the estimated BRS and FRS for the year I turn 55:

BRS: $201,100

FRS: $390,300

My goal is to achieve the required FRS in my combined OA and SA accounts by age 55. Anything above that is a happy bonus! I am aiming for the FRS because the property pledge + BRS method is not my cup of tea. I find it too complicated to maneuver. What if I want to sell my house and live with my kids? Or migrate overseas? Pledging your property may make sense for some people, but I do not like the restriction on decision making and would like to avoid being in that situation.

Is it realistically possible to achieve the estimated FRS of $390k in my OA and SA accounts by age 55 without any additional CPF contributions? Let's find out.

Applying the same assumption of 3% p.a. growth to my salary up till age 40* and by extension, CPF contributions, I should be able to obtain at least $390,300 in my combined OA and SA by age 44. By 65 years of age that would have accumulated to 1.1 million. So the FRS is attainable as long as I continue working till age 55 and CPF does not revise their interest rates downward!

*I am assuming here that past age 40, I am unable to compete with younger folks and my salary stays stagnant.

Using the checkbox above, you can switch between two scenarios.

- I work till age 55, with all housing loan payments paid off. OA + SA at age 65 = 1.1 mil

- I stop working at age 48 and finance the remaining monthly house loan payments (if any) by cash or in a lump sum payment. In this scenario, OA + SA at age 65 = 905k

At age 55, savings in the SA and OA are transferred into the Retirement Account (RA), up to the FRS, with the SA taking priority. If the SA has sufficient funds to meet the FRS, funds from the OA will remain where they are. Based on the first scenario where I work till age 55, there should be 200k in my OA after the FRS has been set aside. This remaining CPF savings will be one source of my retirement income between ages 55-64, before the CPF Life payouts start. If I stop working at age 48, my CPF savings will be quite meager after setting aside the FRS. This is not ideal but it helps to know that at the very least, I need to work till age 48.

The CPF Retirement Funds Calculator

I arrived at the above figures using a calculator I created on an excel spreadsheet. It takes into account existing CPF allocation rates and interest rates based on your age and up to 1 housing loan. Use the calculator to project the funds in your OA, SA and MA accounts up till age 65.

Please read the first "Readme" tab and make a copy of the spreadsheet (File > Make a copy) to start your calculations! I would love to hear your feedback on the calculator, so feel free to leave a comment below 😀

Part 2 of my retirement plan has been published!

29 Apr 21 - Updated some numbers and charts