%20Drawdown%20on%20investment%20capital.png)

Welcome to part 3 of my three-part series where I share about my retirement plan!

- Central Provident Fund (CPF): Maximize that "free" interest to build your retirement savings

- Supplementary Retirement Scheme (SRS): Short-term liquidity vs Long-term growth

- Investment Portfolio

Overview: I plan to use my CPF monies as the most basic level of retirement funds (via CPF Life) from age 65 onwards. The monthly payouts will then be supplemented by withdrawals from my SRS account and dividend payouts (and drawdown on investment capital if necessary) from my investment portfolio.

Investment Portfolio: Meet evolving needs over time

Let's take a pause here and take stock of the first two parts of my plan. You may have noticed that funds in my CPF and SRS account will only become available to me at age 65 (via CPF Life payouts) and 62 (SRS). Assuming all goes well (i.e. there are no health scares and I can continue working till at least age 47), I should have additional CPF savings in my OA, after the FRS has been set aside, that I can withdraw starting from age 55.

Which brings us to the question: Where will I get my living expenses between age 47 (assuming I stop working) and age 55 or potentially, up till age 62? I'm hoping that full-time employment is not a financial necessity after age 47. If I do work, I would like it to be entirely voluntary! This is where I see the dividend component of my investment portfolio playing a key role.

%20Drawdown%20on%20investment%20capital.png?width=800&name=Dividend%20income%20SRS%20withdrawals%20CPF%20Life%20CPF%20Savings%20(OA)%20Drawdown%20on%20investment%20capital.png)

This was a difficult post to write. When I tried to flesh out this 3rd part of my retirement plan, it became clear to me that I have not been investing with any strategy for the past 3+ years. Any gains I've made have been due to pure luck and mostly good choices. If I had not decided to dollar cost average (DCA) into Mapletree Industrial Trust in 2016 and Ascendas REIT in 2017, I would not be sitting on the capital and dividend gains that I have today.

Moving forward, I aim to be more conscious and strategic about my investing decisions so as to achieve my portfolio goals. In the very short-term, my new year's resolution for 2020 is to increase my portfolio value to 70k. I should be able to achieve this comfortably, assuming there is no market crash in 2020 and none of the companies I invest in go bankrupt lol.

I have decided to split my portfolio into a basket of dividend stocks and a basket of value/growth stocks. Presently, my portfolio is approximately one-third value/growth, two-thirds dividend stocks. In 2020, I'll be investing a 50:50 split into each basket. In the following years, I see myself making adjustments to that ratio although I expect that I'll eventually favor dividend stocks for their lower volatility.

Dividend Stocks

I matched my personal criteria for dividend stocks to technical conditions that I could use to build a screener in my Stocks Cafe account.

- Low price volatility: Low beta, low estimated shortfall

- Not too expensive: PE should be lower than sector median

- Earnings resilience: Nett profit margin higher than sector median

- Adequate liquidity for trading

- Overall upwards trend in stock price over past 3-5 years

- Dividend yield of at least 4.5%

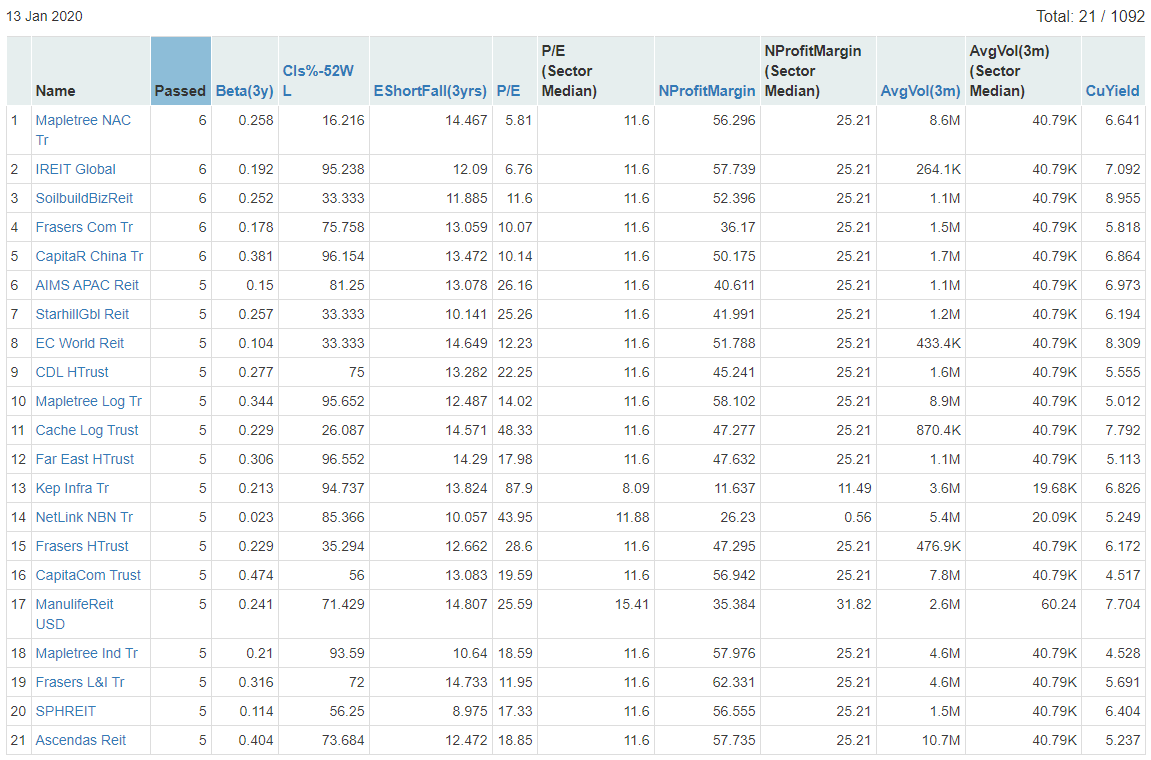

Here is a list of stocks that passed the technical criteria when I ran the screener on 13 Jan 2020

Using the stocks identified with this screener, I did a second filter using qualitative considerations and some personal preferences such as:

- Positive outlook for the next 3-5 years (eg. upcoming or recent acquisitions to boost earnings)

- Strong sponsor (eg. REITS) or very low likelihood of significant losses excluding extraordinary circumstances (eg. DBS, OCBC, UOB)

- Prioritized stocks with lower beta

From the list above, I cut it down to a handful of stocks: Ascott REIT, Netlink Trust and Mapletree Commercial Trust. Since I have limited monies in my warchest to invest, my first pick is Netlink Trust for its recurring streams of income, Ascott REIT for the potential upside post-merger and Mapletree Commercial Trust comes in last because I think the recent acquisitions and Liang Court rejuvenation have already been priced in.

Since these stocks are going into the Dividend basket of my portfolio, I am mainly focused on dividend gains here, less so about potential capital gains from a run up in share price. Considering that these REITS have solid properties/assets, a competitive advantage, plus their low volatility and earnings resilience, I'm quite confident that these stocks will trend upwards in the long term anyway.

Before the start of every quarter, I'll use the screener to shortlist potential stocks to add to my shopping list. Whichever stock's entry point is met, I'll add them to my dividend portfolio, using the savings I've set aside plus any dividends accumulated over the past quarter. Over time, I hope to see the value of this portfolio compound with reinvested dividends (much like what Dividend Warrior has done)!

Value/Growth Stocks

As for the value/growth component of my portfolio, I am currently invested in two technology stocks listed in the US, one of which I'm an employee of. Every month I also have some money going into two Dimensional Funds via MoneyOwl.

One of the biggest reasons I've decided to do a 50:50 split between Dividend and Value/Growth stocks is because I have a nifty employee benefit called an Employee Stock Purchase Plan (ESPP). It basically allows me to purchase my company's stock at a discounted rate. Since the company is operating in a pretty competitive space, the stock is 3-4 times more volatile than the volatility limit I've set for my dividend stock screener and the share price can drop more than 30% if investors are spooked. However, the company is still growing so I reckon the probability of a sustained drop in the stock price significant enough to erode away the discount is quite unlikely. Since its a "free" discount, of course I'll gladly take it!

I view this component of my portfolio as a bet on value picks that can supercharge my portfolio value many times faster than stable dividend stocks can. Its also one way I'm trying to diversify my portfolio outside of local stocks.

In sum, I have the next 2 decades or so to increase the size of my portfolio and its resulting dividend income so as to support myself and my family when I'm in my 40s and 50s. Will I be withdrawing from my investment portfolio in my retirement years? Honestly, I do not know. Someone has written that the fundamental problem with the 4% rule for early retirement isn't the 4% rule, but the underlying assumption of level spending over time. I highly recommend checking out the linked article which is written by a retired couple who are in their early-mid 40s.

I reckon it is too early for me to be crunching numbers for an imaginary passive income when my portfolio is so tiny right now, so I'll be doubling down on increasing my invested capital.

Happy investing y'all 😎